Statement of Activities for Not-For-Profit Entities: Purpose, Objectives & Preparation

Content

- Resources created by teachers for teachers

- Study concepts, example questions & explanations for CPA Financial Accounting and Reporting (FAR)

- Example Question #10 : Not For Profit Accounting

- Grants, Contracts, and Similar Agreements: Sponsored Funding

- Fall Enrollment Totals

- How to Interpret a Cash Flow Statement

- A Beginner’s Guide to Nonprofit Financial Statements and Reports

When you subtract the company’s liabilities from its assets, you are left with owner’s equity. The owner’s equity represents a company’s net worth and is a very important variable for shareholders, current investors, and potential investors. A cash flow statement reports on a company’s cash flow activities, particularly its operating, investing and financing activities over a stated period. The rules used by U.S. companies is called Generally Accepted Accounting Principles, while the rules often used by international companies is International Financial Reporting Standards . In addition, U.S. government agencies use a different set of financial reporting rules.

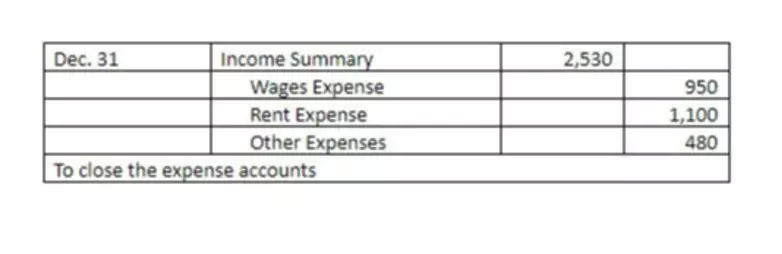

These include sales and the various expenses incurred during the stated period. The net effect of the revenues, expenses, gains, losses and reclassifications is labeled change in net assets. The change in net assets must be the same as the difference between the beginning and ending balance of net assets as reported in the statement of financial position. Nonprofits must compile their statement of activities to be in accordance with the generally accepted accounting principles . This statement can be incredibly helpful when nonprofits are analyzing their finances and trying to determine where those hard-earned fundraising dollars seem to disappear to. While for-profits need to compile a profit and loss statement along with their income statement, nonprofits can skip that step because they’re not operating for profit. The statement of activities is simply to show how the organization is using its revenue and expenses to support its mission.

Resources created by teachers for teachers

The date at the top of the balance sheet tells you when the snapshot was taken, which is generally the end of the reporting period. Your nonprofit statement of activities is split into several different sections. Meanwhile, horizontally, it’s split into your organization’s unrestricted and restricted revenue. By analyzing your nonprofit’s statement of activities, your organization can determine if the expenditures currently allocated for each of your programs are sustainable for the long run. You can use the information in this statement to better understand if now is the right time to cut expenses, provide membership discounts, or secure additional funding through grants or sponsorships. Operating activities detail cash flow that’s generated once the company delivers its regular goods or services, and includes both revenue and expenses.

To learn more about nonprofit accounting check out our nonprofit accounting standards page. The most significant source of revenue for most nonprofits is contributions received.

Study concepts, example questions & explanations for CPA Financial Accounting and Reporting (FAR)

This amount represents the transfers of funds from temporarily restricted net assets to unrestricted net assets resulting from the satisfaction of donor-imposed stipulations concerning timing or purpose. Accounting outputs are financial statements that detail the financial activities of a business, person, or other entity. If you can read a nutrition label or a baseball box score, you can learn to read basic financial statements. If you can follow a recipe or apply for a loan, you can learn basic accounting. The purpose of the change in net assets is to articulate the net assets or equity of the statement of financial position. Income and expenses on the income statement are recorded when a company earns revenue or incurs expenses, not necessarily when cash is received or paid. Similarly, the depreciation of owned assets is added back to net income, as this expense is not a cash outflow.

At GrowthForce, we specialize in helping for-profit and non-profit organizations keep their finger on the financial pulse, so they can focus on what really matters – achieving their greatest potential. Non-profit and for-profit businesses have many similarities, but they also differ in specific areas. For-profit businesses report to shareholders and investors, whereas non-profits report to a Board of Directors or other governing authority. When it comes to bookkeeping for non-profits, many of the processes remain the same as in the for-profit world; however, differences in terminology will apply when managing a charitable organization’s books. The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co., Inc. , offers investment services and products, including Schwab brokerage accounts. Its banking subsidiary, Charles Schwab Bank, SSB , provides deposit and lending services and products.

Example Question #10 : Not For Profit Accounting

https://www.bookstime.com/ for capital projects, endowments, and similar funds are reported as non-operating revenues. A pledge is recorded at the present value of estimated future cash flows, based on an appropriate discount rate determined by management at the time of the contribution. Contributions or gifts include outright cash gifts and pledges to the university. These contributions, including unconditional promises to give, are recognized as revenues in the appropriate categories of net assets in the periods received. Government entities need financial statements to ascertain the propriety and accuracy of taxes and other duties declared and paid by a company. The next line subtracts the costs of sales from the net revenues to arrive at a subtotal called “gross profit” or sometimes “gross margin.” It’s considered “gross” because there are certain expenses that haven’t been deducted from it yet.

- Financing activities generated negative cash flow or cash outflows of -$35.4 billion for the period.

- Pension plans and other retirement programs – The footnotes discuss the company’s pension plans and other retirement or post-employment benefit programs.

- Instead, negative cash flow may be caused by expenditure and income mismatch, which should be addressed as soon as possible.

- It’s called “net” because, if you can imagine a net, these revenues are left in the net after the deductions for returns and allowances have come out.

- Additionally, a balance sheet will show what is called owner’s equity (also known as stockholder’s or shareholder’s equity).

- Vendors who extend credit to a business require financial statements to assess the creditworthiness of the business.

The organization’s bank statements should be reconciled on a monthly basis by someone who does not issue or sign checks on behalf of the organization. In addition, copies of checks, wire transfer information, and other information relating to deposits and withdrawals should be maintained along with the monthly statement. Checks and other expenditures should be examined to verify that the payments are consistent with the organization’s activities and that the expenditures were appropriate. Similarly, deposit activity should also be reviewed to ensure that it corresponds to expected revenues. For example, if the organization held a fundraising event that generated cash, the reviewer should look to see that there are cash deposits that correspond to the event. If the organization banks online, it should still be sure it is regularly downloading or printing and storing its bank statements, deposit slips, check images, and similar documents.

Grants, Contracts, and Similar Agreements: Sponsored Funding

Typically Statement of Financial Activitiess “overhead costs,” including operational expenses that don’t specifically relate to executing your mission or fundraising. The expense section reports all cash that flows out of your organization, including pending expenses—those you know you’ve incurred but haven’t spent the money yet, such as payroll for hours worked the previous month. Having negative cash flow means your cash outflow is higher than your cash inflow during a period, but it doesn’t necessarily mean profit is lost. Instead, negative cash flow may be caused by expenditure and income mismatch, which should be addressed as soon as possible.

Financial Audit: FY 2022 and FY 2021 Consolidated Financial … – Government Accountability Office

Financial Audit: FY 2022 and FY 2021 Consolidated Financial ….

Posted: Thu, 16 Feb 2023 20:00:00 GMT [source]

Financial statements are also read by comparing the results to competitors or other industry participants. By comparing financial statements to other companies, analysts can get a better sense on which companies are performing the best and which are lagging the rest of the industry.

Fall Enrollment Totals

The net assets featured on your nonprofit statement of activities are simply your expenses subtracted from your revenue. This calculation shows the equity of your nonprofit organization and whether you have the revenue to cover expenses, creating a sustainable organization. While for-profits focus on making as much income as possible to make more money for themselves, nonprofit organizations focus instead on how they can raise additional revenue to further their missions. All of a nonprofit’s funds should be reinvested into the organization and its mission. A nonprofit statement of activities example will have a heading, body, and bottom line.